Within the public sector, these variables may be less clear and require more forethought to define, says Rose. “Thinking about how we interpret overall coverage in the private sector, for instance, you might think in terms of income statements or balance sheets and dissect the main drivers of income. For the public sector, however, I would be looking at what major services our department, agency, or cabinet is providing to the public and the metrics around those services — funding, budgetary requirements, expectations that are supposed to be provided under that budget authority, etc. It is just a slight twist to how to map out what the expectations are.”

It is important to note that often in the public sector many of the areas under the assurance coverage of the internal audit function are non-financial in nature. While qualitative measurements (such as governing body satisfaction) are essential, relying on them exclusively as an objective measurement is difficult. Especially in the public sector, it is critical to have processes in place that provide ongoing measurements. The use of a periodic survey that measures citizen or governing body satisfaction over time, for example, allows the internal audit function to track trends, identify areas for improvement, and adapt to the risks and priorities of the organization or agency. The Performance Measurement Tool offers examples of stakeholder survey questions that can be used to create a quantitative performance metric over time.

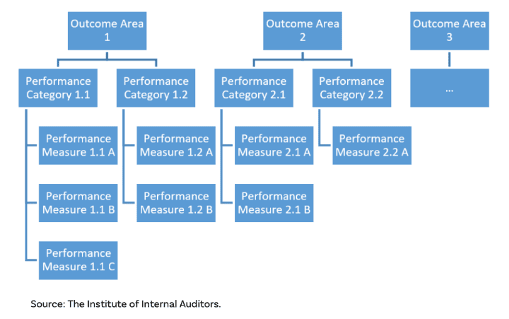

Establishing stakeholder expectations is a critical element of any performance evaluation, but in the public sector, it is especially important due to the multiple stakeholders in play. Performance measures should clearly align with the expectations of the stakeholders. “Your job as a chief auditor,” says Rose, “is to understand what stakeholders individually care about and, to the best of your ability, synthesize everything based on that, including your performance metrics.” The Performance Measurement Tool offers several sample performance measures that could be used to determine stakeholder satisfaction.

Stakeholder expectations will also help determine the best way performance measure results should be reported. The tool offers detailed examples of two different approaches an internal audit function can take: the dashboard and the weighted scorecard. Both approaches have merit, and the ultimate decision on how to present findings should be made by the CAE, based on clear alignment with the needs and expectations of the stakeholders.

A Tool to Enhance Current Performance Measurement Processes

Performance measurement is not a new concept for public sector internal audit functions, and in many jurisdictions, it is required by law. But even for the most mature functions, there is still value in reviewing the Performance Measurement Tool. No process is beyond improvement, and as the risk environment grows in complexity, an internal audit function cannot afford to be caught unaware if one aspect of its services is found lacking. Conformance is important, but it is not enough.

“It's not just about establishing a baseline for conformance; it's about ongoing improvement,” says Pamela Powers, director of professional guidance, public sector, at The IIA. “The only way we can get better is through performance measures. Our goal is to have our members look at this new tool as something that can have real positive value in improving the communication with stakeholders.”

Explore more of the Performance Measurement Tool on the IIA website.