Working within a digitally transformed workforce will require a new way of looking at one’s internal audit career.

The future is bright for internal auditors who develop skills valued in digitally transforming organizations.

Articles Bryant Richards, CIA, CRMA, CMA, Mike Jacka, CIA, CPA, CPCU, CLU Apr 08, 2024

The future is bright for internal auditors who develop skills valued in digitally transforming organizations.

The word is out that organizations are using robotic process automation (RPA) and artificial intelligence (AI) to improve their processes. Results from these deployments show great promise, but the impact of these tools on the future workforce remains unclear. The one question on every internal auditor’s mind: “Will I be replaced?”

The answer seems to be both “no” and “yes.” According to Moving Internal Audit Deeper Into the Digital Age – Part 3, from the Internal Audit Foundation and Deloitte, “Digital tools such as scheduled scripts, RPA, and AI should not operate in silos, but rather they should work in tandem with the internal audit organization as a ‘digital workforce.’” This leads to an important follow-up question: “What will it be like to work alongside that digital workforce?”

According to Generative AI and the Future of Work in America, by McKinsey Global Institute, “Technological advances often causes disruption — but historically, they have eventually fueled economic and employment growth.” This appears to be true with the internal audit profession, but the disruption aspect is where it gets complicated.

Understanding what might occur begins with examining labor forecasts from the U.S. Bureau of Labor Statistics that incorporate trends in RPA:

Although the Bureau of Labor Statistics numbers include some impact of emerging technologies, McKinsey Global Institute provides a deeper analysis, layering on the impact of generative AI, providing more nuance regarding RPA’s impact on internal auditing, and complicating the issue in the process. According to Generative AI and the Future of Work in America, generative AI will put internal audit jobs in the top 10 declining occupations by 2030 — approximately 600,000 fewer bookkeeping, accounting, and audit clerks and 100,000 fewer accountants and auditors.

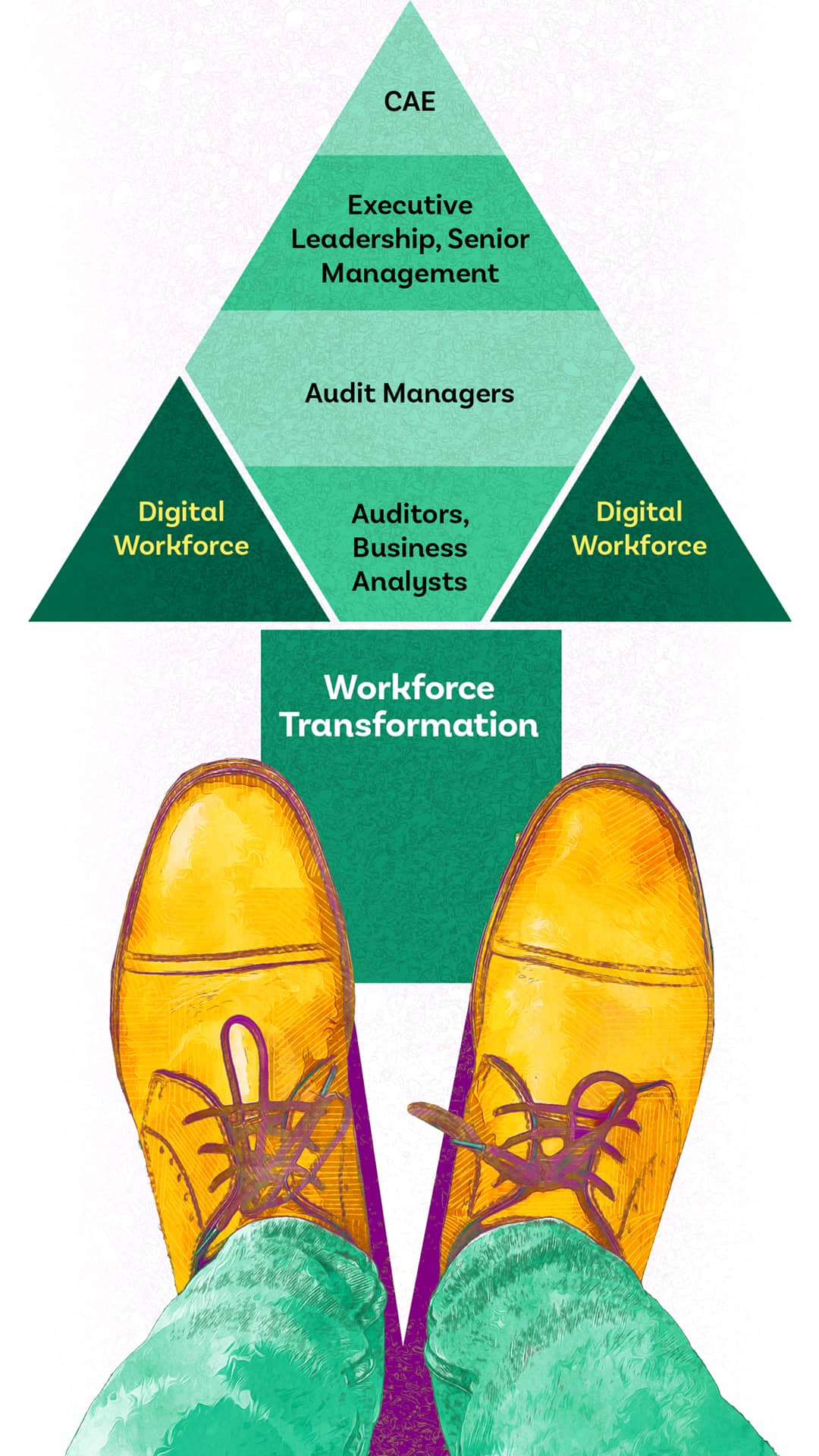

Moving Internal Audit Deeper Into the Digital Age provides a new organizational staffing model for internal audit that corroborates the estimates offered by McKinsey. The Workforce Transformation model (see below) provides insight on how some staff and manager roles will be replaced by the digital workforce.

In many ways, this scenario remains promising for internal auditors. But working alongside a digital workforce provides a disruptive complication that is entirely new to the profession and requires a different way of considering one’s career within internal auditing.

RPA and associated technologies have the power to transform internal auditing and, over time, likely will. However, this transformation will require a shift in the work performed by internal auditors, which may impact their employability. So how will those within the profession respond? How will individual internal auditors and their departments use RPA and AI to continually add the value promised clients, taking that value to the next level? And more to the point, how do internal auditors maintain their roles and future-proof their careers?

In 2015, Thomas Daven-port and Julia Kirby wrote “Beyond Automation,” with the poignant subtitle “A Strategy for Remaining Employed in an Era of Very Smart Machines,” in the Harvard Business Review. Within the article, they presented the Five Paths of Employability framework, based on a concept they called “augmentation strategy.”

“Automation starts with a baseline of what people do in a given job and subtracts from that,” the authors wrote. “Augmentation, in contrast, means starting with what humans do today and figuring out how that work could be deepened rather than diminished by a greater use of machines.”

The result is a set of strategies people can use to understand the possibilities for working with emerging technology, realigning their contributions to the new ways work is done. This framework offers insights into how human contributions will continue to create value in a digitally transformed workplace.

Adapting Davenport and Kirby’s framework to the world of internal auditing illuminates how internal auditors can increase their value to clients in a future that heavily leverages RPA and AI. Whether an auditor is strong in all categories or just one, the model provides insights on how skills will be valued in a digitally transformed organization, and how internal auditors can enhance those roles for themselves and their departments.

Leadership has always been about thinking strategically, considering the big picture, overseeing operations, and leading teams. However, in the age of digital transformation, leadership now includes an understanding of how technology will change the department and helping the department adapt to that change. This is a role that technology likely won’t usurp. It may be able to crunch numbers in ways that support leaders, but it cannot yet think strategically, motivate a team, or resolve conflict.

This does not mean that everyone who pursues this path must be a CAE. Instead, it means that people who embrace this approach recognize leadership opportunities at any level — leader, supervisor, manager, director, etc. Whether pursuing a path toward a CAE role or leveraging time in internal audit to gain skills for other leadership roles, the long list of leadership skills will hold its value.

To succeed as a leader, individuals will need to develop skills such as strategic development, personnel development, motivation, and business acumen. Experienced leaders also point to the important developmental opportunities internal audit offers, such as project management, communicating to all levels of stakeholders, and supporting other team members. Further, the individual who really wants to grow in this area should start exploring certifications, as well as the advantages in pursuing a master of business administration and other post-graduate studies.

Volunteering on IIA boards and committees also can help develop leadership skills. Lastly, mentorship is a common and successful approach to learning the more nuanced steps on this challenging path.

Citizen developers see opportunities for RPA and AI within their own department, learn those technologies, and apply them to improve overall operations. This is the role for individuals within internal audit who want to build automation solutions. They will understand how the programs work and embrace the role of those programs in making the department better.

But these individuals are more than just solution developers. They also use their internal audit knowledge — risks, controls, etc. — to help monitor and modify technology solutions within the department, ensuring the stability of the programs. Once programs are built, it is their responsibility to ensure the programs work as planned. Further, these individuals will keep track of the changes in the programs, incoming data, and surrounding processes and make sure outputs still provide internal audit the information it needs. These people are critical to future internal audits that involve assessing and monitoring the risks of these technologies used outside the department.

The ability to take on this role requires knowledge of the data and technologies used to design and build the programs, but it also requires analyst skills to understand how changes to the programs will affect the output. And, of course, it requires the ability to adapt the risk, control, and process analysis skills learned as an internal auditor to the development of applications.

Those building and running data analytics programs already have many of the needed skills. Experience and training with new tools such as RPA or generative AI will build upon the needed analysis, digital literacy, and problem-solving skills, upgrading existing data analysts to citizen developers.

Within every organization there are specialized areas where it is unreasonable for technology to do the work — specific areas of knowledge where the time and effort involved in building solutions to mine that information outstrips the rewards. Some people relish the role of being the absolute expert, even in a narrow field. This is the person who makes a name by going a mile deep and an inch wide.

The challenge can be finding a niche so specialized it can’t be mechanized, but still important enough for the organization to need that information. Within internal audit that niche may be the need for deep knowledge in a specific process or department, for example, marketing or human resources. The individual would become the go-to individual whenever someone on the team is working around or with those areas.

Another example is regulatory compliance. While there are programs that can identify new rules and regulations, the person whose niche is regulatory issues can take the deep dive to see connections in those regulations that others and computers might not see, and they can interpret those changes in terms of risk and potential audits.

The training and knowledge necessary for this role depends very much on the niche. The experience needed includes an understanding of the organization and how that niche is an integral part of its success. The individual should pursue extensive study and training in that field of specialty, including keeping ahead of evolving trends.

People who identify with this role are those who continue to concentrate on the core work of internal audit with a focus on soft skills — the uncodifiable skills that are not purely rational. These people develop the interpersonal and intra-personal abilities that separate internal audit work from the tasks that can be automated. This role represents working with AI and RPA, using the information they provide, combined with the internal audit soft skills, to provide the value inherent in every audit.

Soft skills make internal auditors more successful in all areas. Even a process as basic as interviewing provides an example of how the audit and risk specialist uses soft skills that cannot be reproduced by RPA. Good interviewing requires experienced auditors who are good at communicating and relating to others. Combine these with the intuition developed by experienced auditors, and they can tell when the truth is being told, when the truth is being bent, and when the truth has left the room. All audit processes require such intuition and the related practices that underlie such intuition. These individuals enhance the team, bringing these uncodifiable strengths to all situations.

Those working in this role will start with a solid understanding of the processes and applications that exist in internal auditing and risk management. They also will need to continually strengthen the soft skills — emotional intelligence, relationship management, change management, ability to communicate — and people and psychological skills that are the human part of internal auditing. These attributes allow the internal auditor to understand the actions and reactions of those with whom they are working.

This role combines traits of both the leader and the citizen developer. This is the technology expert who always wants to be on the cutting edge. It also is the visionary leader who studies, predicts, and envisions the future that new technologies allow, up to and including designing and implementing those new technologies. As Davenport and Kirby put it, this person is “bringing about [the] machines’ next level of encroachment.” They are not afraid of what technologies can do; they are helping determine what they will do next. They are finding a future that does not yet exist.

For internal audit, these will be the individuals who not only help determine how best to use the tools but also are looking for the next tools. They will figuratively be trying to put internal audit out of work — finding new and better ways for machines to get the audit work done. But in the process, they will be continuing to help internal audit develop new skills and approaches. They will be looking for the work computers cannot do while finding ways computers can accomplish those tasks, all toward internal audit providing more value to its customers.

As with the citizen developer, this role requires technological skills and the need to understand use case identification, program deployment, and technology governance. This individual also should be at the forefront of new technology, exploring new use cases. And, this person will need to develop and enhance leadership traits such as creativity, innovation, strategy development, and vision.

There are overlaps among the five categories. So, heading in one direction does not preclude understanding and practicing aspects of another. Successful approaches will likely include a multitude of combinations and depths. Recognizing the different approaches helps one understand how to best move forward. All internal auditors should assess which step(s) best suits their skills, interests, and desire for advancement. Working with internal audit leaders, auditors can look for opportunities to enhance their skills in the desired path.

Understanding and applying roles also is important for internal audit leaders. While each leader will need to understand his or her path, there are two other considerations. First, leaders should work within the department to ensure everyone is going down a path that best suits them. Talent development is an important part of any leader’s job, and helping auditors find the opportunities to grow, providing them feedback, and freeing the resources for this to be accomplished is paramount. Second, leaders should look at the makeup of the department. Considering a combination of these five paths within each department is a key to success. Of course, small audit functions will not have this luxury. Those leaders should still identify the gaps and determine how they might be filled from elsewhere in the organization.

Technology is bringing new challenges and opportunities to the world of internal auditing. As clicking keys becomes stripped from work activities, opportunity opens to create more value. Continuous learning, working with technology, critical thinking, flexibility, and resourcefulness will become more important than ever. The future is bright for internal auditors who develop skills valued in digitally transforming organizations.