On the Frontlines: The Power of Branding

Blogs Ricardo Correa Fuenzalida, CIA, CGAP, CCSA, CRMA Aug 05, 2025

The internal audit function in the public sector faces ever-increasing expectations: greater transparency, efficiency, and integrity. In this challenging environment, internal audit must position itself as a strategic and trusted ally for its stakeholders. A powerful, yet often underestimated, tool is branding. Not in the commercial sense, but as a means to strengthen purpose, build trust, and shape perceptions of internal audit.

What is Branding in Internal Audit?

Branding, in its broadest sense, refers to the deliberate process of shaping and managing the identity, reputation, and perception of an organization or function among its stakeholders. In the commercial world, branding involves names, logos, and marketing, but in the context of internal audit, branding means much more than visual elements. For internal audit, branding is the sum of what the function stands for — its core values, ethical standards, commitments, and the unique promise it makes to the organization. Effective branding ensures that internal audit is not only recognized for what it does, but also for why it does it and the value it brings. In practical terms, internal audit branding is about consistently communicating the function’s purpose, principles, and impact, creating a recognizable and trusted identity that fosters credibility, engagement, and alignment with the public interest.

Beyond Perception: Branding as a Vehicle for Purpose

Although internal audit is not a commercial brand, it does possess an organizational identity: values, practices, commitments, and a mission that must be recognized and valued. Branding, in this context, means communicating our institutional value and purpose: providing independent assurance, reliable advisory services, and promoting continuous improvement.

When the purpose of internal audit is communicated clearly — through coherent messaging, a consistent visual identity, accessible language, and strategic presence — it ceases to be viewed merely as a compliance entity and is recognized as a generator of trust and valuable insights.

Practical Suggestion:

Consider developing a “Value Proposition” for your internal audit function: a clear commitment to stakeholders about the unique benefit they can expect. It answers the question: Why should you trust us?

Example Value Proposition:

“Internal audit provides independent assurance, generates reliable insights, and promotes continuous improvement in public management, strengthening trust in the institution and in the use of public resources.”

Building Institutional Trust: The Critical Intangible

Public organizations face intense social and political scrutiny. In this context, stakeholder trust (board, senior management, citizens, oversight bodies) is essential. A deliberate focus on branding strengthens this trust, presenting internal audit as approachable, valuable, and acting with integrity.

Practical Suggestion:

Establish a regular communication channel, such as a quarterly digital newsletter, where internal audit shares key achievements, improvements, and results in accessible and visually engaging language. A well-designed audit newsletter, focused on results and impact for the organization, can transform perceptions of technical reports into stories of public transformation. A recognizable logo or institutional tagline, aligned with public service values, can foster belonging and credibility.

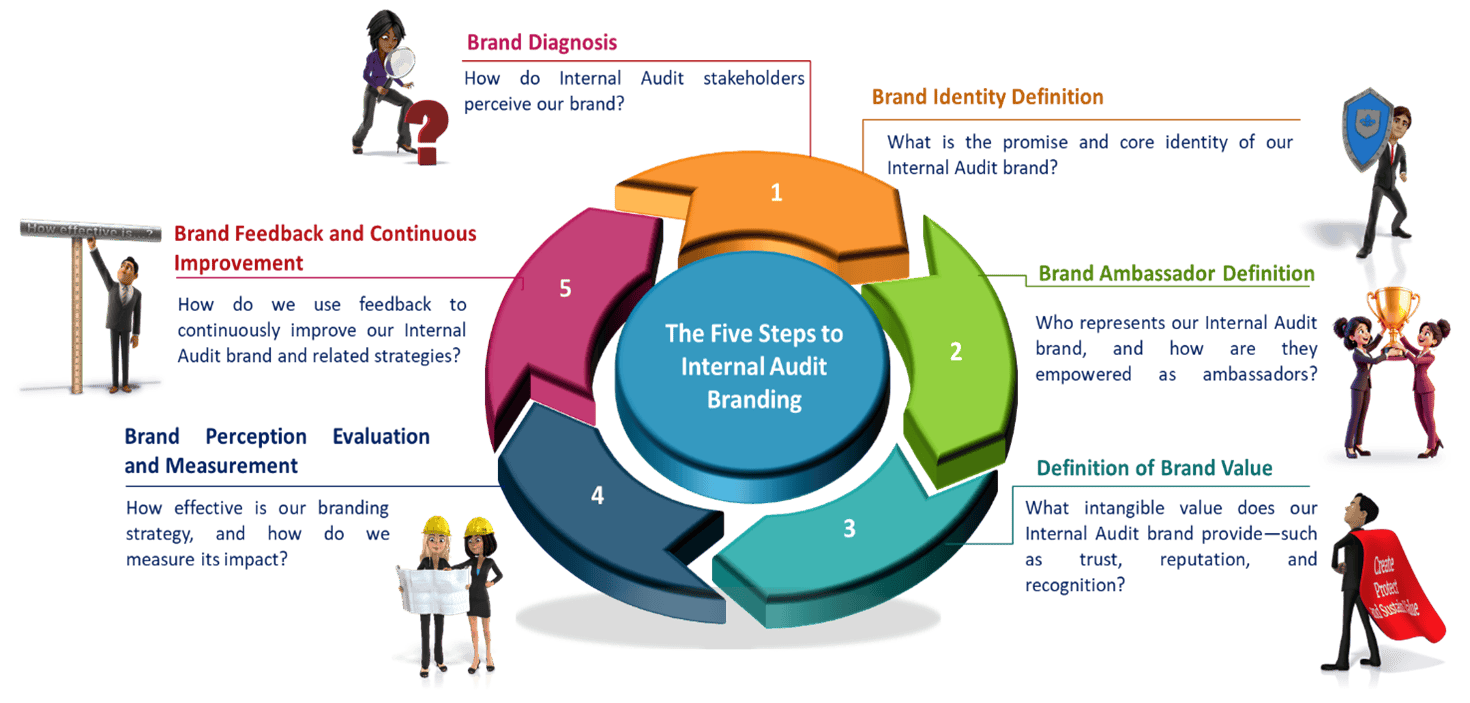

Five Essential Steps to Developing a Branding Strategy for Internal Audit in the Public Sector:

1. Diagnose and Define the Internal Audit Brand

Begin by assessing how stakeholders — including the board, senior management, staff, and the public — perceive the internal audit function. Use surveys, focus groups, or perception studies to understand both current perceptions and the legitimacy attributed to internal audit within the organization. Based on these insights, establish a clear and compelling “value promise” that articulates who internal audit is and what it offers its stakeholders. The brand identity must be authentic and aligned with the mission, values, and unique strengths of the internal audit function. This forms the foundation for building trust and relevance.

2. Identify and Empower Brand Ambassadors

Ensure all internal audit team members are aligned with the established brand identity. Provide training and guidance so that staff become engaged, consistent, and credible spokespersons for the internal audit function — both within the organization and externally. Effective brand ambassadors help reinforce positive perceptions and build internal credibility.

3. Define and Enhance Brand Value

Enhance the internal audit brand by demonstrating and communicating intangible value elements such as trust, reputation, and recognition. Showcase how internal audit adds value through its independence, insight, and contributions to effective governance and public resource stewardship.

4. Evaluate Brand Perception and Drive Continuous Improvement

Regularly measure the effectiveness of branding strategies using specific metrics and key performance indicators. Seek feedback through perception surveys, stakeholder interviews, and qualitative assessments. Use these insights to refine and adjust branding strategies, ensuring continuous improvement and increased alignment with stakeholder expectations.

5. Brand Feedback and Continuous Improvement

Use feedback from previous steps to continuously refine, adjust, and improve the brand identity and related strategies.

Branding Is Not Marketing

It is critical to clarify: Branding in internal audit is not about promotion or advertising. It is a strategic tool for managing purpose and trust. The goal is not to appear infallible, but to demonstrate reliability, usefulness, and alignment with the public interest.

In times of fragile public trust, internal audit teams with clear purpose and a strong identity become pillars of effective governance. Well-managed branding ensures that stakeholders not only understand what internal audit does, but also believe in why it does it.

The views and opinions expressed in this blog are those of the author and do not necessarily reflect the official policy or position of The Institute of Internal Auditors (The IIA). The IIA does not guarantee the accuracy or originality of the content, nor should it be considered professional advice or authoritative guidance. The content is provided for informational purposes only.

Learn more with our other resources

Articles

Fraud: The Heartbreaking Fraud

Articles

Basics: Persuasive Results

Articles

Editor’s Note: The Next Leaders

Articles